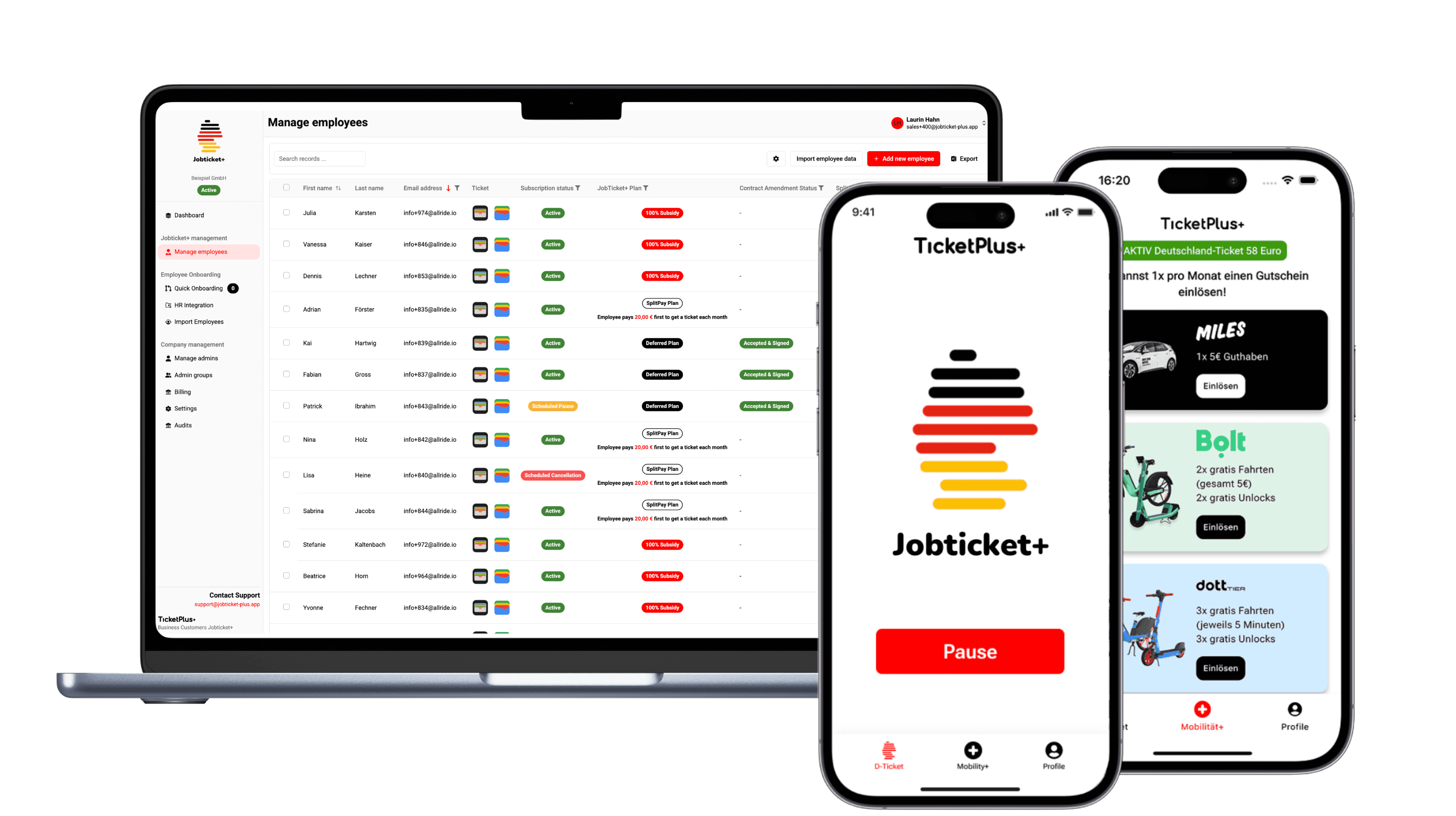

Salary Conversion – Free for the Company. Actually Profitable.

Your employees receive the Deutschlandticket through salary conversion – as employer you don't just pay €0, you effectively earn €1.71 per employee per month.

SV savings of €12.92 minus flat-rate tax (€10.21) and service fee (€1) result in a net profit for the company.

Instead of €63 for a private purchase, employees effectively pay only €37.67 net through the conversion – a monthly saving of over €25.

The legally required addendum to the employment contract is automatically generated via Jobticket+ and digitally signed. Zero HR overhead.

How salary conversion works

In salary conversion, employees waive part of their gross salary (€63 – the full ticket price without discount) to fund the Deutschlandticket. Important: the full €63 – not the discounted price – is used as the conversion amount, as this maximises social contribution savings for the company. The employer flat-taxes this amount at 15% under §40(2) sentence 2 no. 1 EStG. As a result, the benefit in kind remains exempt from income tax and social contributions for the employee. Net income falls by approximately €37.67 – not €63. The tax benefit is in addition to the existing €50/month non-cash benefit allowance.

Example calculation: Costs for employer and employees

Example: Employee with €3,000 gross salary (tax class I, Bavaria, with church tax)

Employer

Employee

All figures are indicative based on general assumptions (SV rate 20.5%, church tax 8%). Please consult your tax advisor for your specific situation. This does not constitute tax advice.

Frequently asked questions about salary conversion

Is salary conversion possible for mini-job employees?+

Do employees need to give their consent?+

What happens when a ticket is paused or employment ends?+

Introduce the Deutschlandticket – €0 cost for your company

No IT knowledge required. Setup in under 5 minutes, tickets issued in 30 seconds. No minimum term, contract addenda generated automatically.