Employer Subsidy – The Tax-Free Salary Boost

You cover the Deutschlandticket in full for your employees – tax-free, no salary negotiation, immediate added value. Employees pay €0. You pay €60.85/month.

The subsidy is fully exempt from income tax and social contributions under §3 No. 15 EStG – including private use of the ticket.

Gross salary and net income remain completely unchanged. The ticket is a pure additional benefit on top.

Unlike salary conversion, no addendum to the employment contract is required. Setup is straightforward.

How the subsidy model works

In the subsidy model (also called 'on-top'), the employer covers the full ticket cost in addition to the regular salary. Under §3 No. 15 EStG, the subsidy up to the ticket value (€59.85) is fully exempt from income tax and social contributions. The €1.00 service fee is a business expense for the employer and does not constitute taxable income for the employee. Employees' net income remains unchanged – the ticket comes entirely on top. For employees who would otherwise buy the ticket privately, this represents a saving of €756 per year.

Example calculation: What does the model cost?

Example: Employee with €3,000 gross salary (tax class I, Bavaria)

Employer

Employee

All figures are indicative based on general assumptions. Please consult your tax advisor for implementation in your specific company. This does not constitute tax advice.

Frequently asked questions about the subsidy model

Is the subsidy model suitable for mini-job employees?+

Can the subsidy model be combined with other non-cash benefits?+

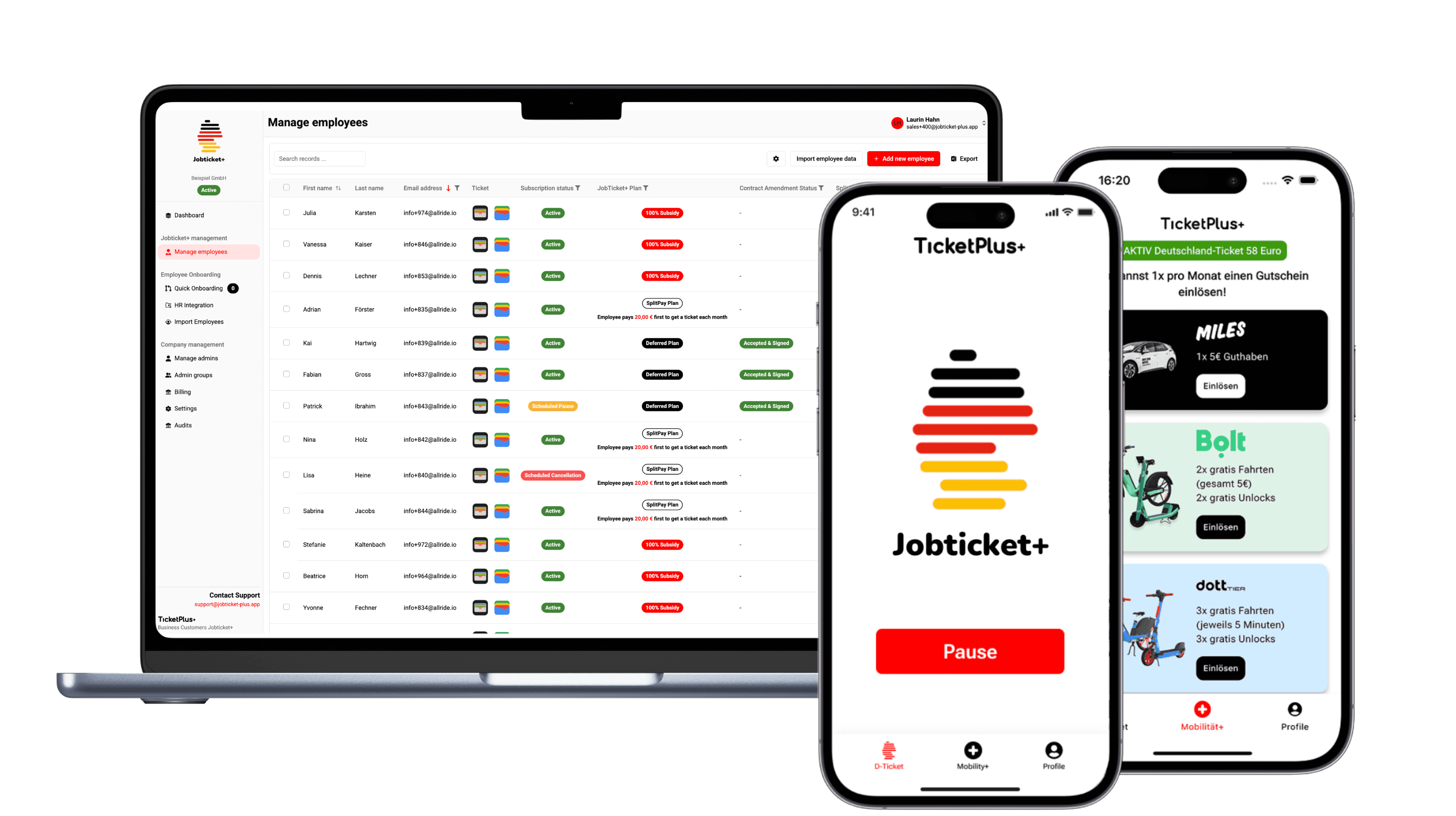

Introduce the Deutschlandticket as a maximum employee benefit

No IT knowledge required. Setup in under 5 minutes, tickets issued in 30 seconds. No minimum term, 50+ HR integrations included.